We start with a simple premise: information technology is cyclical.

The Technology Lifecycle

Every 15 years or so, a fundamentally new computing platform emerges. Markets fluctuate as it develops steadily, reducing production costs to become the new standard. New firms and talent, who can now more effectively compete, move into the space, dropping prices and margins in the process. The size of the market grows as new businesses are built out on top of the new open standard, some of which eventually rise to the top of the industry and leverage their scale to make competition expensive. Eventually, demand for open source, low-cost alternatives reaches a critical point, and the cycle begins again.

This pattern has played out time and time again over the course of recent history: the transistor in the 1950s, the microprocessor and PC in the 1970s, the operating system and the web in the 1990s. Today, we find ourselves in another period of consolidation driven by today’s tech giants, who are leveraging their user networks and proprietary data to make competing with them especially difficult.

Demand for alternatives is rising, as we see clearly in a shift in media sentiment toward these incumbents over the last decade. Just as IBM was dubbed a bestriding colossus in 1983, the very same antitrust argument is nearing a boiling point today.

Cutting through the noise, one thing becomes clear: competing with incumbents is more expensive than it’s ever been. So where might we turn to next?

Cryptonetworks and the Internet

Every time one of these once-in-fifteen-years shifts takes place, the very basis of society’s social, political, and economic systems shift along with it. Critically though, technology evolves over the course of countless iterations.

The first information revolution was the advent of language some 100-thousand-or-so years ago. After the phonetic alphabet greatly expanded the capabilities of written language, we revolutionized its distribution with the printing press, which was followed in increasingly rapid succession by the telegram, telephone, radio, television and internet. The internet, admittedly, is unique: unlike any other information technology, the internet encompasses all of its precedent evolutions. You can watch, text, call, listen, communicate and interact with people and media, even all at once. Pantera Capital’s Co-CIO, Joey Krug, puts it well: “The internet, unlike historical information revolutions, not only revolutionized access to content, it democratized the creation of that content.”

But what does this have to do with crypto? Just as the internet marked a new information infrastructure, crypto marks a new financial infrastructure. For the last 500 years, humanity has broadly operated with 5 major asset classes: government-backed money, equity, debt, real estate, and commodities. Not only has crypto managed to present itself as the first truly new asset class in 5 centuries, it has also managed to encompass all of them. Just as the internet encompassed its precedent information technologies, crypto can represent any of its precedent asset classes digitally.

The notion of a truly new asset class is undoubtedly radical. It’s important to keep in mind, however, that a suggestion is as only as radical as its context. To point back at our analogue in information technology, the value of a printing press, telephone or the world wide web wasn’t immediately apparent: In 1943, Thomas Watson, the president of IBM, famously predicted there’d be “a world market for maybe five computers.”

At first glance, this is all crypto is: a purely economic phenomenon; a supplement or underpinning to the broader information technology called the internet. What I’d argue, though, and what proves central to this overarching thesis is that money itself is information: scarcity and fungibility are just necessary features for it to function as a medium of exchange, a store of value, and a unit of account.

Our traditional approach to working with information is creating copies. On the internet, we copy its origin and send a direct copy, as in a photo, or alter it and send the result, as in a document. Money must be scarce by definition, making our traditional approach impossible. Seeing as the fundamental function of blockchains is keeping track of who-has-how-many of a given token at any point in time, we can come to understand crypto as a new infrastructure for information, and arrive at a simple conclusion. Joel Monegro and Chris Burniske sum up well in their own thesis: “Crypto, basically, is the native business model of networks – which, as it turns out, encompass the entire economy.”

Here, we arrive at the concept of a cryptonetwork— a decentralized information network that is coordinated via a scarce and programmable digital token with an open and defined monetary policy.

The Value of Open Source

The biggest problem with the current state of the legacy internet is its reliance on restricting access to information for profit. Proprietary business models function by accumulating data, then charging users for it directly or indirectly. In their decentralization, cryptonetworks are inherently open source, and usher in 4 fundamental shifts as a result:

Breaking Aggregation Theory

To take a page from Ben Thompson, we can divide a consumer’s value chain into 3 parts: suppliers, distributors, and consumers/users. Optimally, a firm seeks to monopolize one of the three vertically, or integrate two of them to derive an advantage in providing a vertical solution.

Today, suppliers are commoditized by digital platforms. Facebook is supplied by user-generated content, Amazon is supplied by individual retailers, and Spotify is supplied by individual artists. This makes number of users and thus quality of user experience the determining factor for success. This also means digital platforms are effectively aggregators: they control demand, pulling suppliers onto their platforms on their own terms, and tend toward a winner-takes-all scenario by leveraging their scale, creating massive deadweight loss in the process. In this sense, suppliers must bow to aggregators. SEO as a field, for example, is built around commoditizing yourself for Google’s benefit.

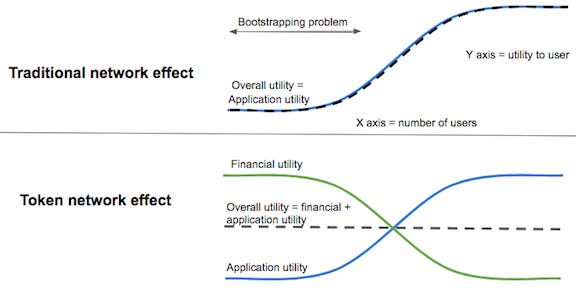

Cryptonetworks break out of this by creating new assets instead of creating market inefficiencies through extractionary relationships with network participants. They accomplish this through a baked-in financial incentive structure that rewards early adopters with network equity in greater magnitudes the earlier they become participants or contributors.

Tokens help overcome the bootstrap problem by adding financial utility when application utility is low. Via The End of Aggregation Theory by Rhys Lindmark. Collapsing Transaction Costs

If the free market is so good at allocating resources, why do firms exist? Ronald Coase sought to answer that question in 1937 in The Nature of the Firm. According him, the optimal size of a firm in any given industry would decrease as transaction costs in that industry decreased. Transaction costs include sourcing, negotiating and enforcing transactions. As Coase saw it, transaction costs were a driving factor for the existence of firms in the first place because those costs were so much lower under one roof as opposed to many individuals trying to freelance with each other.

Cryptonetworks bridge the market and the firm, offering the best of both worlds in the process. Graphically, they push the tradeoff boundary between transaction cost efficiency and incentive maximization outwards. Like markets, they facilitate the organization of decentralized economic activity. Like firms, they help reduce transaction costs. Simply speaking, cryptonetworks allow individuals to collaborate trustlessly from anywhere in the world.

Cryptonetworks push the tradeoff boundary between transaction cost efficiency and inventive maximization outward. Via Cryptonetworks and the Theory of the Firm by Qiao Wang. Strengthening Network Effects

A network effect, simply speaking, occurs when a product or service becomes more valuable as more people use it. We also know this effect as Metcalfe’s Law. Originally applied to telecommunications, it states that the value of a network is proportional to the square of the number of nodes in that network. We’ve seen this effect act as a kingmaker for Web 2.0 platforms and its importance is only heightened today.

Metcalfe’s Law. Via Technopedia. Under cryptonetworks, network effects are strengthened. The underlying reason for this is their ability to capture supply and demand side, starting network effects for applications earlier on by charging and compensating early adopters in native tokens.

In his piece, On the Network Effects of Stores of Value Kyle Samani argues, with the figure below as context, that “...there are no networks that exhibit n^2 network effects... Bitcoin as digital gold will be subject to the perpetually sub-linear log(n) network effect, whereas Bitcoin as digital cash can achieve super-linear network effects as crypto adoption grows from <1% to 50% of the global population.” I believe the analogue for cryptonetworks here is the latter superlinear outcome, and it comes down to adoption. Composability, interoperability, or more simply— the ability for cryptonetworks to support and act as open source infrastructure for applications and for each other means their potential “surface area” of value capture is limited only by the strength of their underlying protocol.

Best case network effects. Via On The Network Effects Of Stores Of Value by Kyle Samani. Re-Defining Ownership

The 2008 Bitcoin whitepaper marked the advent of blockchain computers. The ideas originally proposed by Satoshi Nakamoto have been expanded and iterated on endlessly, but the underlying value of trust arising from the mathematical properties of a system rather than individual network participants themselves has ushered in an era of verifiable collective ownership.

So we can own and help operate internet infrastructure. This might seem trivial at first glance, but, As Jesse Walden puts it, could potentially usher in the next frontier of consumer software. He continues: “Rather than a platform’s inner circle of founders and investors taking home the value, users are able to earn the majority of value generated from their collective contributions.”

The Ownership Economy. Via Variant. This matters because the economics of modern consumer applications is broken. They can’t generate revenue embedded in stock prices and anyone who buys that stock needs to wait many decades for dividends to cover its initial cost. In the attention economy, advertising has become the primary driver of revenue, prioritizing a user’s information over a product or service itself. Cryptonetworks’ enablement of tokenized micro-economies allow for a subtle but important paradigm shift that might act as the cornerstone of the next-generation of software: value is derived not from attention on a platform, but from participation in a network.

Implication: Open Protocols

There’s a very important implication here. Blockchains’ foundation in distributed ledger technology and an open-source architecture for data facilitates something that we’ve seen countless times but have never been able to properly invest in or compensate individuals for: companies built on top of open protocols. Today’s tech giants wrapped Web 1.0 protocols in interfaces that anyone could use intuitively— SMS was the foundation for messaging apps, HTTP for browsers, SMTP for email apps, and the list goes on. Of course, these were all open source protocols with no real mechanism for ownership. Anyone who had hypothetically invested substantially in HTTP in the 90s would be among the wealthiest people, ever.

Crypto protocols allow for the open-source, consensus-driven nature of early web protocols with baked in monetization and composability. Affectionately, people refer to some of them as money legos, but their promise spans well beyond traditional finance. Everything from freelancing, music streaming, communications and wireless networks are fair game.

With this in mind, the crux of our thesis is simple: Investing in open crypto protocols presents the highest implied value capture by maximizing the surface area of potential economic activity.

Investment Fundamentals

With our thesis on paper, it’s important to explore our process for investment. Joey Krug gives us a straightforward formula:

“As an investor, you primarily want to do three things:

Buy the assets and companies that will most effectively enable your investment thesis;

Hold them, buy more when they decline in price or become cheap vs. fundamentals;

Constantly reevaluate #1 and #2, and your thesis”

Beyond the basics, there are two important factors to keep in mind when dealing with investment in cryptonetworks:

The Hype-Innovation Cycle

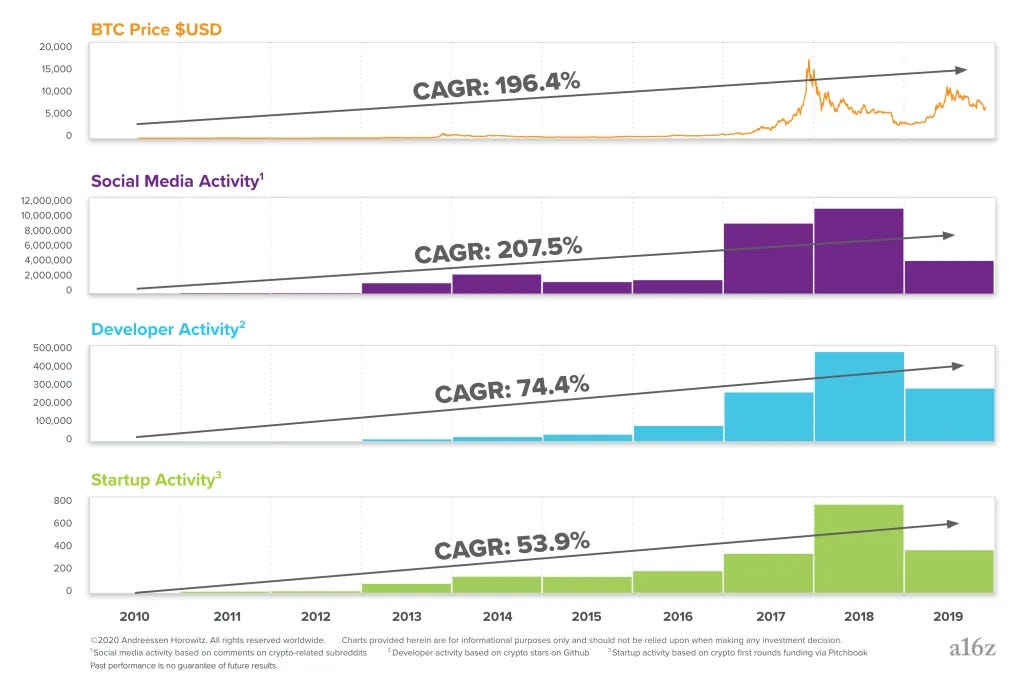

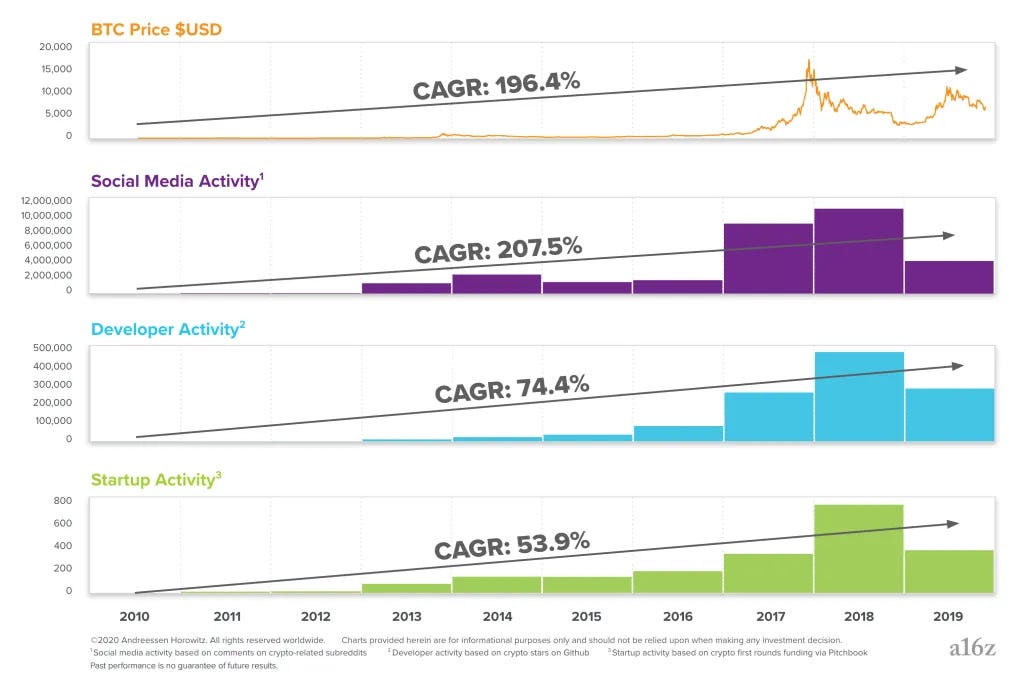

Crypto markets are notoriously volatile. Beyond their historically speculative nature, we can observe, since as early as 2009, a rough 3-step cycle emerges. We’ll use Bitcoin prices as an example.

As the prices of crypto-assets rise, new interest bubbles up across social and legacy media.

More people get involved in the space, contributing ideas and code in the process.

A new layer of infrastructure is built out by these newcomers, setting the stage for another shift in price.

We first saw this in 2009-2012, with Bitcoin reaching parity with the US dollar in 2011. Before this point, only enthusiasts and people deep in the tech world knew Bitcoin existed at all, and even its strongest advocates only saw it as an experiment with little practical value. The spike attracted a new set of talent, who realized real businesses could be built around this new technology. It was at this point that many of today’s largest incumbents, like Coinbase, Kraken and Bitfinex were founded.

2012-2016 saw a peak in late 2013, marking the first time Bitcoin or crypto in general broke out of niche tech circles. The wider media buzz brought a number of developers and projects orders of magnitude greater than the last cycle. Projects like Ethereum and companies like Gemini and Binance were born as a result.

The third cycle took place over the course of 2016-2019, with a 2017 peak marking the point in time when the implications of decentralized finance broke into the mainstream. The frenzy was once again an order of magnitude greater than the last, and birthed projects like Compound, Maker, Celo, dYdX, and more.

The Crypto Price-Innovation Cycle. Via Future from a16z. Critically, according to an a16z study, “...developer, social media, and startup activity is sustained even after prices decline... this is a consistent pattern that leads to long-term steady growth in fundamental innovation.” Simply speaking, price-driven hype is the mechanism by which innovation takes place, but the resultant talent and technology sticks around.

The Technology Cycle

To now take a tech, rather than price-driven approach, we can view cryptonetworks through the lens of any other emerging technology. As mentioned at the beginning of this piece, much of the growth we’ve experienced to date has been driven by the supply side of the market. As Facebook, Apple, Amazon, and Google become harder to compete with, an increased distrust in institutions, lower barriers to entry and outsized returns make crypto’s continued talent inflow not just logical, but probably inevitable.

To take a page from Carlota Perez’s Technological Revolutions and Financial Capital, emerging technologies are broken into 4 phases: Interruption, Frenzy, Synergy, and Consolidation. Crypto has undoubtedly entered a frenzy, and if previous cycles of emerging technologies are any indication, this could last until the end of the decade.

Investing through the technology cycle. Via Placeholder. Of course, timing markets perfectly is notoriously impossible. Crypto reached a $2T market cap in April 2021, and has fluctuated around that point over the last year, but given the borderless nature of these assets, we could still be far from the top.

Similar patterns of speculation preceding the dot-com bubble allowed companies to raise at inflated valuations, propping themselves up on venture capital rather than fundamentally sound business models. Cryptonetworks are different in this regard, which Joel Monegro and Chris Burniske point out: “A significant correction can take out large chunks of the supply side of a network (as happened to a lot of Bitcoin miners following the coin’s 85% drop in 2013 and 2014), but as long as one node continues to spin, the protocol lives on. This insight shows the importance of selecting properly decentralized systems with the right cryptoeconomic models when investing with a long time horizon. These are the ones that will thrive during the frenzy, persist through the crash, and scale throughout the deployment phase of crypto.”

When dealing with these kinds of long investment time horizons, it’s important to keep in mind that cryptonetworks don’t necessarily die in the same way traditional startups do.

With that in mind, the key lies in building a portfolio that lasts through the probable set of corrections ahead of us, opting to dollar-cost-average investment in open protocols that act as infrastructure for sets of decentralized applications, rather than playing games of pure speculation investing directly in what’s built on top of them.

On Buying and Selling

With the market’s cyclical nature in mind from both a price and technology standpoint, we find that investing in an all-weather manner is an advantage. The underlying infrastructure that presents the most sound investment opportunities is born in the post-boom troughs most shy away from.

In addition, it’s probably unreasonable not to take a generalist attitude toward investment within the confines of our thesis. Given the potential of open protocols to transform such a wide range of industries, the answer might be taking a wider view.

When it comes to deciding when to sell, dealing in crypto comes with its distinct set of advantages. Unlike traditional venture, the inherently liquid nature of tokens allows for the possibility of early exits from bad investments. Options range from simply selling one’s position in the open market to helping fork a network if the protocol and community are sound, but core developers aren’t up to par. In an ideal and more common scenario however, exits should simply take place once the underlying thesis of a project has been realized.

For a space that moves so quickly, it’s important to have some go-to heuristics to fall back on. Good investments boil down to being contrarian and right, and I feel this rough thesis acts as a good starting point for making them as the future unfolds before us.

Thanks for reading,

Alex

SOURCES:

A Crypto Thesis by Joey Krug

Aggregation Theory by Ben Thompson

Bitcoin: A Peer-to-Peer Electronic Cash System by Satoshi Nakamoto

Breaking down public trust by Rebecca Cohen

Composability is Innovation by Linda Xie

Cryptonetworks and the Theory of the Firm by Qiao Wang

How many computers does the world need? Fewer than you think by Nick Carr

Money Legos And Composability As DeFi Building Blocks by Vincent Tabora

On the Network Effects of Stores of Value by Kyle Samani

Placeholder Thesis Summary by Joel Monegro and Chris Burniske

Technological Revolutions and Financial Capital by Carlota Perez

The Colossus That Works by John Greenwald

The End of Aggregation Theory by Rhys Lindmark

The Ownership Economy: Crypto & The Next Frontier of Consumer Software by Jesse Walden

The case against Big Tech by Sara Morrison and Shirin Ghaffary

Webvan And Other IPO Epic Failures via Investopedia

What’s Next in Computing? by Chris Dixon

Why Decentralization Matters by Chris Dixon

Network Effects and Global Domination: The Facebook Strategy by Fred Vogelstein

The Crypto Price-Innovation Cycle by Chris Dixon and Eddy Lazzarin

The Ownership Economy: Crypto & The Next Frontier of Consumer Software by Jesse Walden